Europe Plant Based Meat Market Size

The europe plant based meat market size was valued at USD 1.56 billion in 2024 and is anticipated to reach USD 1.80 billion in 2025 from USD 5.85 billion by 2033, growing at a CAGR of 15.85% during the forecast period from 2025 to 2033.

Plant based meat is food product engineered from legumes, grains, fungi, or novel proteins to replicate the sensory and nutritional attributes of animal derived meat without involving slaughter or livestock farming. According to the Global Food Innovation, 32% of European households purchased plant-based meat at least once in 2024. The European Commission Farm to Fork Strategy positions reduced meat consumption as integral to achieving the EU’s climate-neutrality goal by 2050, thereby elevating plant-based alternatives as strategic instruments in dietary transition. According to sources, households in countries such as Germany, the Netherlands and Spain were among the most frequent buyers of meat-substitute products in recent years. The European Food Safety Authority approved the use of mycoprotein and precision-fermented proteins in novel food applications during 2023, which is expanding the ingredient base beyond traditional soy and pea proteins. Cultural shifts are also evident and broader consumer research has found a significant share of younger Europeans cite environmental concerns as a motive to reduce red-meat intake. Unlike generic vegetarian products, modern plant-based meats emphasise texture, heme-content and culinary versatility to appeal to flexitarians rather than strict vegetarians, which is marking a distinct evolution in product philosophy and market targeting.

MARKET DRIVERS

EU Climate and Dietary Policy Frameworks Catalyse Product Adoption

The binding policy architecture of the European Union linking food systems to climate action serves as a primary driver of the European plant-based meat market. According to the Joint Research Centre, the livestock sector accounts for approximately 14.5% of the EU’s total greenhouse-gas emissions. The Sustainable Food System Framework requires EU member states to integrate dietary guidelines that cap weekly red-meat consumption at 300 g per person by 2030, aligning with the Global Methane Pledge commitment to reduce agricultural emissions by 30 % by 2030. The policy context means that reducing meat consumption is seen as essential. In response, national dietary plans in Germany and Denmark now formally recommend plant-based alternatives as primary protein sources. Furthermore, in France the EGalim law mandates that school-canteen meals must progressively shift toward higher plant-based protein content and lower red-meat content, transforming plant-based meat from a niche choice into a policy-supported mainstream option across institutional and retail channels.

Rising Prevalence of Lifestyle Related Chronic Diseases Spurs Health-Conscious Consumption

Health concerns linked to excessive red and processed meat intake are further boosting the expansion of the European plant-based meat market. According to the European Cancer Information System, approximately 361,986 new cases of colorectal cancer were recorded in the EU in 2022. The World Health Organization has classified consumption of processed meat as carcinogenic to humans (Group 1). According to the European Heart Network, more than 1.8 million deaths in the EU are attributed to cardiovascular diseases each year. In response to these health risks, a pan-European survey found that about 51% of meat-eating Europeans reported they are reducing their annual meat intake. Modern plant-based meat alternatives aim to address these concerns by offering lower saturated fat, zero cholesterol, and added fiber. For example, pea-protein products may contain around 70% less saturated fat than ground beef. Moreover, as per the research by the European Food Information Council, 61% of health-conscious European shoppers regard plant-based meat as a functional food supporting long-term wellness, not merely an ethical substitute.

MARKET RESTRAINTS

Persistent Sensory and Textural Gaps Limit Mass Market Appeal

Many plant based meat products still fail to replicate the mouthfeel, juiciness, and flavor complexity of conventional meat, which is deterring habitual meat eaters from sustained adoption and impeding the growth of the European market. According to a 2023 review of plant-based meat analogs, a significant portion of sensory studies report that many consumers perceive these products as lacking juiciness, firmness or realistic meat-like bite. For example, the review noted that plant-based meat analogs “lack of juiciness, elasticity and firmness”. Practical sensory research confirms these deficits with texture and flavour fidelity remaining key obstacles in market conversion. The challenges are particularly pronounced in whole-muscle analogs (such as steaks or chicken breasts) where fibrous structure remains difficult to engineer without expensive extrusion or fermentation techniques. Consequently, repeat purchase rates for some plant-based meat alternatives lag due to unmet sensory expectations. Until texture and flavour fidelity improve at accessible price points, plant-based meat will struggle to convert core meat consumers beyond the flexitarian fringe.

Ingredient Sourcing Volatility and Supply Chain Fragmentation Increase Production Costs

The reliance on a narrow set of protein crops primarily soy, pea, and fava bean exposes the European plant-based meat sector to agricultural instability and import dependency, which is further hampering the regional market expansion. According to the European Commission’s Agricultural Market Observatory, the EU imported an estimated 15.9 million t of soybeans/soybean-meal in 2020, of which Ukraine alone accounted for nearly 40% of an identified subset. The heavy reliance on overseas supply, particularly for non-GMO soy is leaving the feed, food and alternative-protein value chains vulnerable to geopolitical disruption and freight inflation. Domestic cultivation of high-protein pulses remains constrained and as EU data show protein crop production reached only about 4.32 million in 2022 (up from ~4.27 million in 2021), representing a very modest area share. Supply-chain inefficiencies further compound the challenge as the lack of vertically-integrated extraction, texturization and formulation systems increases input-cost burdens. A recent study by Wageningen University estimated that fragmented sourcing in alternative-protein supply chains can inflate input costs by approximately 18% to 22% compared to vertically coordinated animal-meat chains. Taken together, these structural constraints undermine price competitiveness and scalability of plant-based protein supply within the EU.

MARKET OPPORTUNITIES

Expansion into Foodservice and Institutional Catering Unlocks Volume Growth

The integration of plant-based meat into restaurants, cafeterias, and public sector meal programs represents a high potential opportunity for market expansion beyond retail. According to the European Environment Bureau, about 30% to 40% of food service procurement contracts in the EU now include recognised sustainability criteria under public tender frameworks. The revision of the European Union Green Public Procurement (GPP) Criteria for Food and Catering Services embedded in the wider European Commission’s Sustainable Food System Framework directs that public institutions must integrate sustainable criteria, such as lower-impact protein sources into food tenders, thereby enabling plant-based options to qualify for green-procurement scoring. In Germany, the Federal Ministry of Food and Agriculture reports that over 1,200 university canteens now serve plant-based meat weekly, which is reaching over 2 million students. Major restaurant chains are also driving trial. For instance, the McDonald’s McPlant burger has achieved permanent-menu status in several European countries after successful pilots indicated uplift in younger demographics. Similarly, Compass Group Europe is committed to sourcing 30 % of its protein from plant-based sources by 2026 across its client-sites. This institutional channel not only boosts volume but normalises plant-based meat as a mainstream culinary choice rather than a specialty item.

Advancements in Precision Fermentation Enable Next Generation Protein Innovation

Emerging biotechnologies, particularly precision fermentation are unlocking novel proteins that overcome the functional and sustainability limitations of traditional plant source, which is a significant opportunity in the European plant-based meat market. According to the European Food Safety Authority (EFSA), the number of scientific opinions on novel food applications in the EU reached 117 by the end of 2023. The approval of several mycoprotein and precision-fermented protein ingredients enables commercial use across the EU. Companies like Enough Foods in the Netherlands are advancing production of mycoprotein with significantly lower land-use intensity compared to traditional soy-based proteins, as supported by the Joint Research Centre’s life-cycle assessment database. Facilities such as Mycorena’s Promyc plant in Sweden are scaling to industrial capacities by supplying texture-rich bases for whole-cut analogs. Fermentation-based operations can also co-locate with renewable energy sources, as illustrated by the partnership between Nestlé and Solar Foods in Finland. This technological leap positions Europe to lead in high-fidelity, low-impact meat alternatives beyond the first-generation extruded products.

MARKET CHALLENGES

Consumer Scepticism Regarding Ultra Processing and Clean Label Expectations

A growing segment of European consumers views plant-based meat as overly processed and inconsistent with clean label preferences, which is creating a perception barrier to mainstream acceptance and is one of the considerable challenges to the expansion of the European market. According to a 2024 survey, 65% of Europeans reported concern about the health implications of ultra-processed foods. Many current plant-based burger formulations are perceived as complex or artificial. For instance, 63% of respondents across Europe expressed concern about ingredient lists in plant-based burgers, particularly when terms like “methylcellulose” or “yeast extract” appear. The European Food Information Council emphasises that transparent and simple ingredient lists are now key to consumer trust. In France and Italy, where whole-food culinary traditions are strong, only about 22% of consumers regard plant-based meat as “natural”. This scepticism is amplified by media narratives that call into question the supposed health halo of meat analogues. Until formulations simplify without compromising functionality, plant-based meat risks remaining confined to urban, tech-savvy demographics rather than achieving broad cultural resonance.

Regulatory Ambiguity Around Labeling and Terminology Creates Market Confusion

The absence of harmonized EU rules governing the naming and marketing of plant-based meat products fuels consumer uncertainty and legal friction with traditional meat sectors, which is also challenging the growth of the European market. According to a 2024 study by the European Sensory Science Society, 49% of Danish consumers reported uncertainty about whether plant-based products actually contain meat because of ambiguous packaging cues. The European Court of Justice (ECJ) ruled on 4 October 2024 that EU Member States cannot prevent manufacturers from using terms traditionally associated with meat such as “burger”, “sausage” or “steak” for plant-based foods unless the terms are legally defined at national level. In parallel, the ECJ’s 2017 ruling in case C-422/16 clarified that purely plant-based products cannot use the designations “milk”, “cream”, “butter”, “cheese” or “yogurt” that are reserved for animal-derived products. The resulting regulatory patchwork where countries like France impose term bans while Germany adopts self-regulatory guidelines creates complexity for pan-European branding and increases compliance costs for manufacturers. Without clear, science-based labelling standards that balance transparency and innovation, the market faces continued friction that impedes consumer trust and cross-border scalability.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Product Type, Source, Distribution Channel, and Region. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, the Czech Republic, and the Rest of Europe |

|

Market Leaders Profiled |

Beyond Meat, Inc., Impossible Foods Inc., Kellogg Company, Quorn Foods Ltd., VBites Foods Limited, Maple Leaf Foods Inc., The Vegetarian Butcher, Gold&Green Foods Ltd., Plant & Bean Ltd., Taifun-Tofu GmbH, Heura Foods, and Rügenwalder Mühle Carl Müller GmbH & Co. KG.. |

SEGMENTAL ANALYSIS

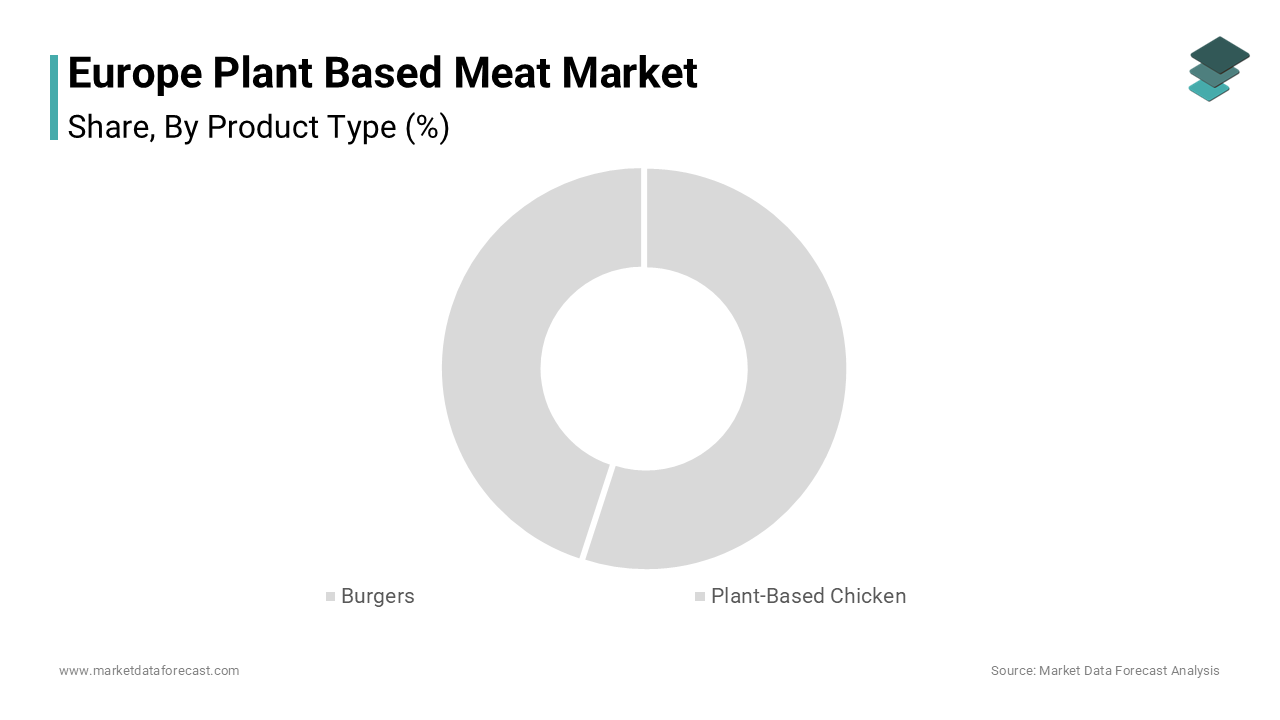

By Product Type Insights

The burgers segment accounted for 37.7% of the European market share in 2024. The growth of the burgers segment is primarily driven by their established presence in fast food and retail channels and integration into mainstream fast-food menus normalizes consumption. Plant based burgers have achieved unprecedented visibility through strategic partnerships with major quick service restaurants across Europe. The plant-based burger offering from McDonald’s called McPlant has been rolled out in several European markets. According to sources, the Burger King Rebel Whopper was made available in around 2,500 outlets across 25 European countries. This mainstream placement reduces trial barriers and reframes plant-based meat as a culinary choice rather than an ethical compromise. According to the European Commission’s guidelines on sustainable food procurement, public institutions are encouraged to include plant-based burgers in cafeteria offerings. This dual penetration cements the burger as the gateway product for flexitarian adoption and is contributing to the expansion of the burgers segment in the European market.

The plant-based chicken segment is projected to expand at a CAGR of 19.9% over the forecast period in the European market owing to the high per capita poultry consumption creates a large addressable base. According to Eurostat data, the average annual consumption of poultry meat in Europe is approximately 23 kg per person. Unlike beef that faces strong environmental stigma, poultry is often perceived as a lean and moderate protein, which is making its plant-based counterpart appealing to health-conscious flexitarians rather than just vegans. In the UK and Spain, where chicken is a dominant meat in the diet, plant-based versions offer a low-friction substitution. According to a European consumer survey, 36% of those who reduced meat consumption replaced red meat with poultry or poultry alternatives. Brands like Revo Foods and Vly have capitalised on this by launching shredded and nugget formats that mirror everyday cooking applications such as stir fries, salads and sandwiches and thereby aligning with existing meal routines rather than requiring behavioural change.

By Source Insights

The soy segment had the leading share of 41.4% of the European market share in 2024 due to its functional versatility and established supply chains. Superior functional properties enable diverse product formulations of soy is also driving the domination of soy segment in the European market. Soy protein isolate and concentrate offer unmatched water-binding, emulsification, and gelation capabilities critical for replicating meat textures across formats. Soy is widely recognised in the EU plant-based sector as a primary protein owing to its ability to form fibrous networks during high-moisture extrusion. The functional robustness of soy allows manufacturers to produce consistent, shelf-stable products across temperature and pH variations, which is making it a go-to choice for large-scale production despite rising competition from newer proteins.

The pea protein is anticipated to witness the fastest CAGR of 21.4% over the forecast period in the European plant-based meat market due to the allergen free positioning appeals to sensitive consumer segments. According to the European Academy of Allergy and Clinical Immunology (EAACI), soy allergy affects approximately 0.3% of European adults and 0.5% of children, which is leading many households to avoid soy-containing products entirely. The status of pea protein as a non-allergen under EU Regulation 1169/2011 gives it a decisive advantage over soy, which is a top 14 allergen requiring mandatory labeling. Brands like Heura and Meatless Farm have leveraged this by formulating 100% pea-based lines marketed as “soy free” and “hypoallergenic,” which is capturing health-focused shoppers. According to the European Consumer Organisation (BEUC), 58% of parents with food-allergic children prefer pea-based alternatives, creating a loyal niche. This safety perception, combined with neutral flavor and high digestibility are primarily driving the growth of the pea protein segment in the European market.

By Distribution Channel Insights

The supermarkets segment occupied the major share of 53.5% of the regional market in 2024. Supermarkets serve as the primary access point for mainstream consumers. Strategic shelf placement in meat aisles drives impulse and trial purchases in supermarkets is one of the key factors driving the domination of the supermarkets segment in the European market. European retailers have increasingly moved plant-based meat from vegetarian sections into refrigerated meat aisles by normalizing it as a direct substitute. Brands like Heura and Meatless Farm have leveraged this by formulating 100% pea-based lines marketed as “soy free” and “hypoallergenic,” which is capturing health-focused shoppers. This contextual integration reduces stigma and leverages existing shopping routines, which is making substitution effortless. Retailers also use promotional bundling, such as “buy one beef, get one plant-based free to encourage trial without requiring ideological commitment, thereby expanding the consumer base beyond core vegans.

The food service segment is growing rapidly and is estimated to showcase a CAGR of 23.4% over the forecast period in the European plant-based meat market due to the mandatory public sector sustainability procurement. European legislation now compels public institutions to prioritise low‑carbon food options, directly benefiting plant‑based meat in cafeterias and canteens. European public procurement criteria for food services emphasise a shift towards a diet richer in fruits, vegetables, legumes, whole grains, nuts and seeds, while reducing red and processed meat. In Sweden, free hot school lunches are provided to all students aged 7‑16 (and most aged 16‑19) five days a week and the national guidelines emphasise eco‑smart meals. Similarly, French universities have significantly increased the proportion of vegetarian dishes in dining halls thanks to institutional efforts. These institutional contracts provide stable volume demand for manufacturers and normalise consumption among younger demographics, which is creating long‑term behavioural shifts that extend beyond the cafeteria.

REGIONAL ANALYSIS

Germany Plant Based Meat Market Analysis

Germany dominated the plant-based meat market in Europe in 2024 by holding 23.9% of the regional market share. The mature vegan culture and industrial food innovation ecosystem of Germany are majorly driving the growth of the German market. The leadership of Germany is further driven by the confluence of consumer activism, policy support, and manufacturing capability. According to a survey published by ProVeg and cited in Germany, 40% of Germans describe themselves as flexitarian. The Federal Ministry of Food and Agriculture allocated funding under its national protein strategy to support alternative‑protein startups, which is resulting in a significant increase in production facilities in recent years. Companies like Rügenwalder Mühle and Veganz have achieved national distribution with plant‑based sausages that mimic traditional German bratwurst to ensure cultural relevance. Additionally, Germany’s stringent food‑labeling laws require clear allergen and origin disclosure to enhance consumer trust in plant‑based products. This blend of demand, policy, and product localization are significantly contributing to the domination of Germany in the European market.

United Kingdom Plant Based Meat Market Analysis

The United Kingdom is expected to account for a prominent share of the European plant-based meat market over the forecast period owing to the strong retail innovation and health-oriented consumer trends. European supermarkets in the UK have significantly expanded their private‑label plant‑based meat offerings, positioning themselves as leaders in Europe. The National Health Service (NHS) dietary guidelines recommend that people who currently eat more than 90g of red or processed meat per day reduce it to no more than 70g, in order to lower health risks. London’s status as a culinary hub fosters chef‑led plant‑based concepts; restaurants such as Wulf & Lamb and Club Mexicana have helped normalise meat analogues in mainstream dining. Moreover, the UK’s post‑Brexit regulatory autonomy has enabled faster novel food approvals, allowing heme‑ and mycoprotein‑based products to reach shelves ahead of some EU counterparts. This agile ecosystem of retail, health policy and gastronomy are fuelling the plant-based meat market growth in the UK.

France Plant Based Meat Market Analysis

France held a substantial share of the European market in 2024. The plant-based meat market in France is primarily driven by the public health mandates and culinary adaptation. The EGalim 2 law of France requires school canteens to serve at least one fully plant based meal per week. According to a 2025 survey by the Climate Action Network France, 53% of French people say they have reduced their meat consumption over the past three years. French consumers are becoming increasingly receptive to plant‑based options despite the country’s strong traditional meat culture. Local brands such as Soy and HappyVore have succeeded by tailoring products to French cuisine by offering plant‑based versions of duck confit, saucisson and steak haché that respect gastronomic expectations. The French Agency for Food Safety maintains rigorous clean‑label standards by pushing manufacturers to simplify formulations. This unique fusion of regulatory push, cultural sensitivity and quality expectations are boosting the plant-based meat market in France.

Netherlands Plant Based Meat Market Analysis

The Netherlands is projected to account for a notable share of the European market during the forecast period due to its role as a biotech and logistics hub. Netherlands hosts Europe’s largest alternative protein cluster, including startups like Meatable and Revo Foods that are supported by the Dutch government’s Protein Transition Fund. Rotterdam Port serves as the primary entry point for non-GMO soy and pea imports that enable efficient ingredient distribution across the continent.

COMPETITIVE LANDSCAPE

The Europe plant based meat market features a dynamic mix of global giants local innovators and food conglomerates competing on taste authenticity sustainability and price. Multinationals like Beyond Meat and Nestlé leverage scale and distribution while European startups such as Heura Oumph and Vly differentiate through regional sourcing and culinary relevance. Competition is intensifying around whole muscle analogs and chicken formats as burgers reach saturation in core markets. Regulatory alignment with EU climate and labeling standards has become a critical competitive lever with carbon transparency and clean labels now expected rather than optional. Private label expansion by retailers exerts downward pressure on branded pricing forcing continuous cost innovation. Simultaneously venture capital continues to fund fermentation and precision agriculture startups creating a pipeline of next generation competitors. This multifaceted rivalry drives rapid product evolution but also fragments marketing efforts and complicates consumer messaging across a diverse regulatory and cultural landscape.

KEY MARKET PLAYERS

A few of the major companies in the europe plant based meat market include

- Beyond Meat, Inc.

- Impossible Foods Inc.

- Kellogg Company

- Quorn Foods Ltd.

- VBites Foods Limited

- Maple Leaf Foods Inc.

- The Vegetarian Butcher

- Gold&Green Foods Ltd.

- Plant & Bean Ltd.

- Taifun-Tofu GmbH

- Heura Foods

- Rügenwalder Mühle Carl Müller GmbH & Co. KG

Top Players in the Market

Beyond Meat

Beyond Meat maintains a strong presence in the Europe plant based meat market through its science driven approach to replicating animal meat using pea protein and non GMO ingredients. The company has deepened its European footprint by expanding distribution in major retailers like Tesco, Carrefour, and Edeka while securing permanent menu placements with McDonald’s and KFC across multiple countries. In 2024 Beyond Meat launched a reformulated burger with 35 percent less saturated fat and improved cooking performance tailored to European culinary preferences. It also partnered with the University of Copenhagen to validate the environmental benefits of its products under EU life cycle assessment protocols, reinforcing its alignment with regional sustainability standards and consumer expectations.

Nestlé

Nestlé leverages its extensive European manufacturing and distribution infrastructure to drive adoption of its Garden Gourmet and Incredible Burger lines across retail and food service channels. The company has prioritized clean label formulations, removing artificial additives and emphasizing European sourced pea and soy proteins to meet regional consumer demands. In early 2024 Nestlé inaugurated a dedicated plant based innovation center in Germany focused on texture and flavor optimization for whole muscle analogs. It also integrated carbon footprint labeling on all Garden Gourmet packaging in compliance with the EU Product Environmental Footprint framework. These initiatives underscore Nestlé’s strategy of embedding plant based meat within its broader portfolio of sustainable nutrition solutions across the continent.

Heura Foods

Heura Foods has emerged as a leading European native brand by championing Mediterranean inspired plant based chicken and whole cut products made from non GMO European pea protein. Headquartered in Spain, the company emphasizes transparency, regenerative agriculture, and climate impact reduction as core brand values. In 2024 Heura launched the world’s first carbon insetting program for plant based meat, investing directly in soil health projects to offset emissions across its value chain. It also expanded into 12 new European markets through partnerships with premium retailers like Ekoplaza and Waitrose. By combining local sourcing, culinary authenticity, and measurable environmental action, Heura has positioned itself as a purpose driven alternative to multinational brands.

Top Strategies Used by the Key Market Participants

Key players in the Europe plant based meat market prioritize clean label formulations by eliminating artificial additives and emphasizing non GMO European sourced ingredients to align with consumer preferences. They invest in sensory optimization through advanced extrusion and fermentation technologies to achieve texture and flavor parity with animal meat. Strategic partnerships with major retailers and quick service restaurants ensure mainstream visibility and trial. Companies increasingly adopt carbon footprint labeling and life cycle assessments compliant with EU environmental standards to build credibility. Vertical integration of protein supply chains reduces cost and enhances traceability. Product innovation focuses on culturally relevant formats such as sausages bratwurst and chicken strips to resonate with local culinary traditions. These strategies collectively address taste trust and sustainability imperatives across diverse European markets.

RECENT MARKET DEVELOPMENTS

- In March 2024, Beyond Meat reformulated its flagship burger with reduced saturated fat and enhanced cooking performance specifically for European consumer preferences and strengthen the Europe plant based meat market presence

- In February 2024, Nestlé opened a dedicated plant based innovation center in Frankfurt Germany focused on developing whole cut meat analogs using European pea protein and strengthen the Europe plant based meat market presence.

- In January 2024, Heura Foods launched a carbon insetting program investing in regenerative agriculture projects across Spain and Portugal to offset emissions across its supply chain and strengthen the Europe plant based meat market presence

- In May 2023, Oumph partnered with IKEA Food Services to introduce plant based meatballs in all European IKEA restaurants reaching over 150 million annual visitors and strengthen the Europe plant based meat market presence.

- In April 2023, Vly expanded distribution of its soy free pea based chicken strips to 8000 retail outlets across Germany France and the Netherlands through a deal with Metro AG and strengthen the Europe plant based meat market presence.

MARKET SEGMENTATION

This research report on the europe plant based meat market has been segmented based on the following categories.

By Product Type

- Burgers

- Plant-Based Chicken

By Source

By Distribution Channel

- Supermarkets

- Food Service

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe